Code can be found on Github.

The code generates disaster measure introduced in Siriwardane (2015). A brief explanation for the disaster measure is provided in This note

To construct the disaster measure the code loads data on individual names options, fits Stochastic Volatility Inspired smiles (Zeliade’s white paper) into implied volatilities and isolates the jump component following Du and Kapadia (2012).

Prior research found that small companies are more correlated with real economic activity. A disaster measure constructed from individual names rather than using options of aggregate indices levers this observation. Technical Appendix provides more details on estimation. Details on Replication of Cremers JUMP and VOL factors.

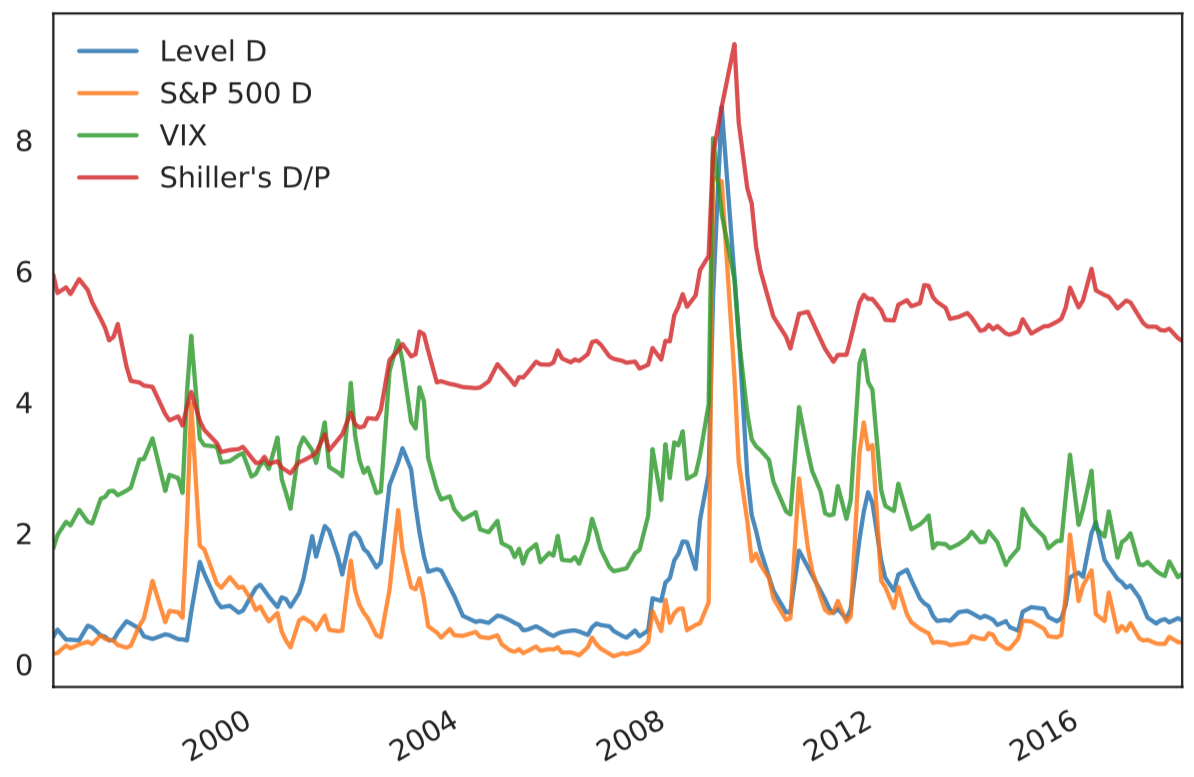

In the two figures below I compare the disaster measure estimated from individual names options (Level D) with disaster measure estimated from options on S&P 500 (S&P 500 D) and with various valuation measures and measures of economic activity

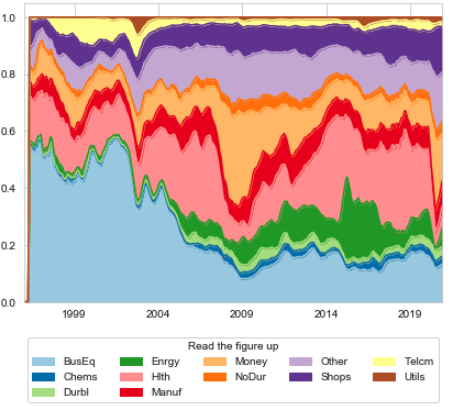

In the Figure below, I show the contribution of different industries to the disaster measure estimated using individual names options. In particular, elevated disaster measure during the DotCom bubble is driven primarily by Business Equipment industry (tech) and in the GFC by Money industry (banks and insurance companies).

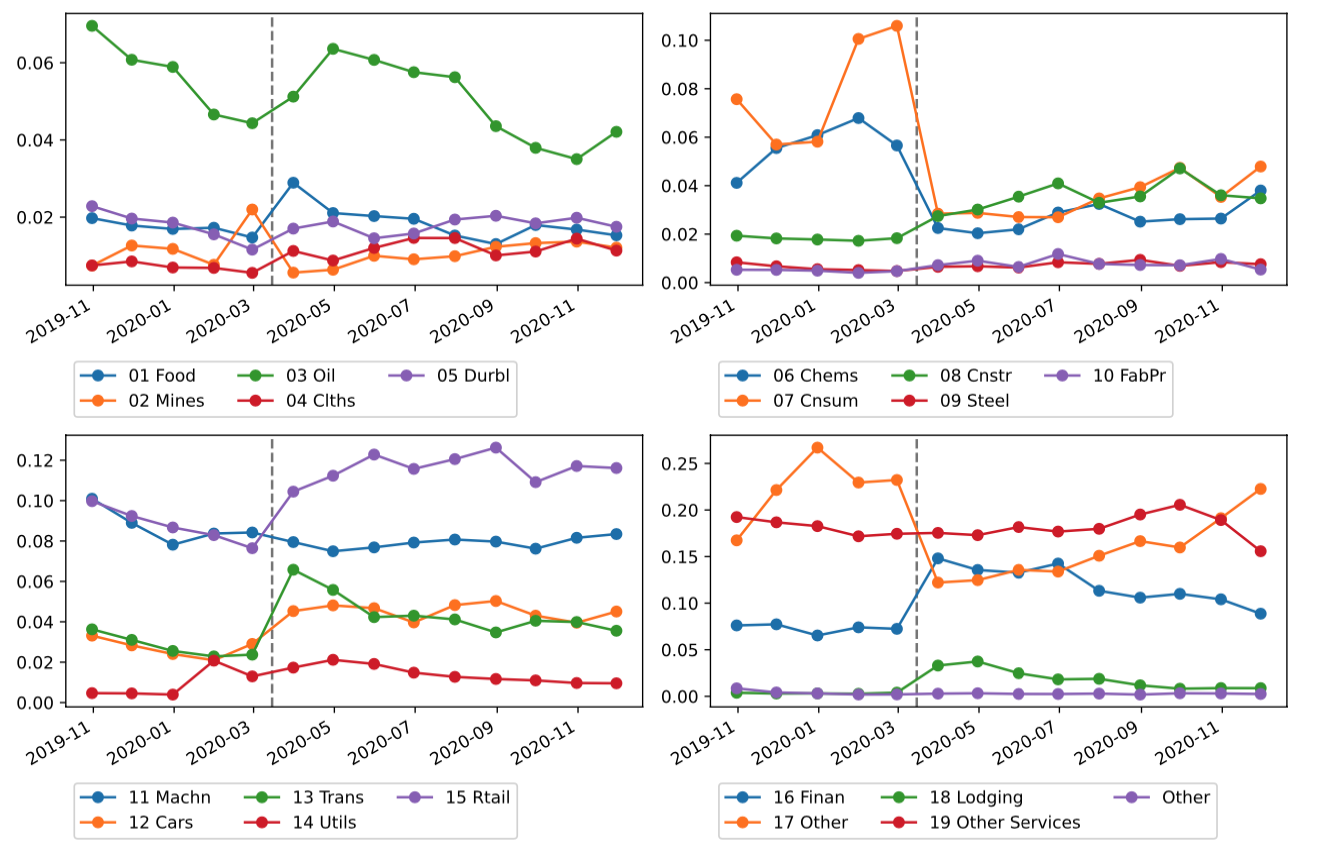

If we zoom in on the industry composition of disaster measure during 2020 presented on the figure below, we can clearly see that contribution of industries that were hit by the COVID pandemic increased in March 2020.

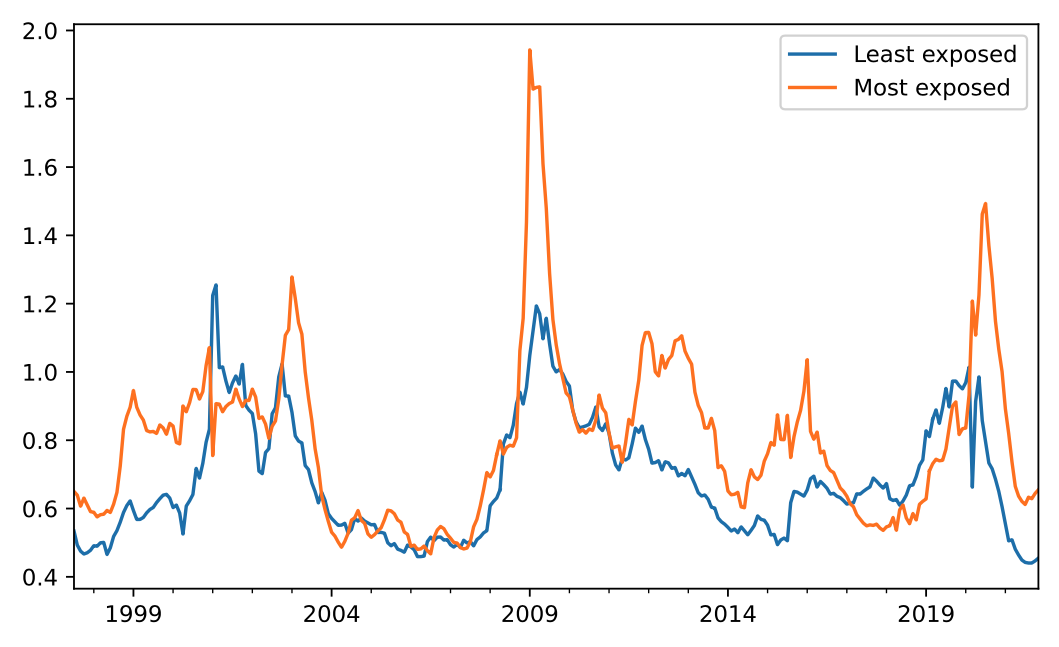

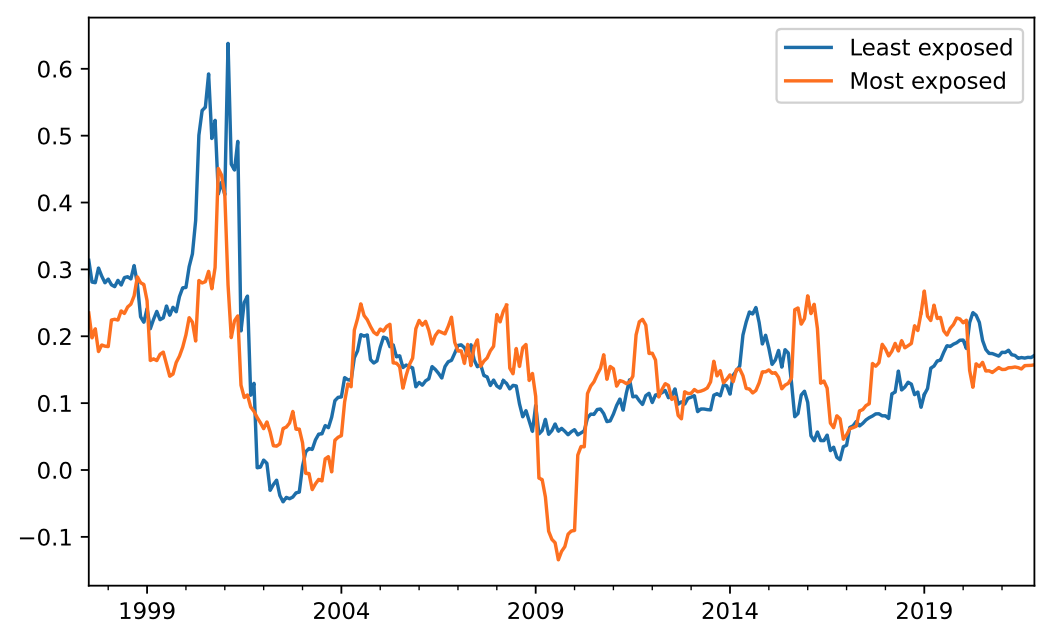

After constructing the aggregate disaster measure discussed above we sort companies on their exposure (beta), form portfolios and compare the average characteristics of the most and least exposed portfolios